Syndic Yourself vous accompagne de A à Z dans votre rôle de syndic bénévole

de charge € pour votre copropriété

à notre plateforme

Syndics bénévoles: nous simplifions votre mission !

Pourquoi faire confiance à Syndic Yourself pour vous accompagner dans votre mission de syndic bénévole ?

Syndic Yourself accompagne les syndics bénévoles de A à Z dans la gestion simple et efficace de leur copropriété. Notre équipe d’experts en comptabilité, juridique et copropriété est disponible pour vous aider en cas de question !

Une plateforme simple et une armée d’experts en comptabilité, droit et copropriété à disposition des syndics bénévoles

Gagnez en temps, argent et énergie

Un service transparent et sans supplément

Une copropriété mieux gérée, tout simplement !

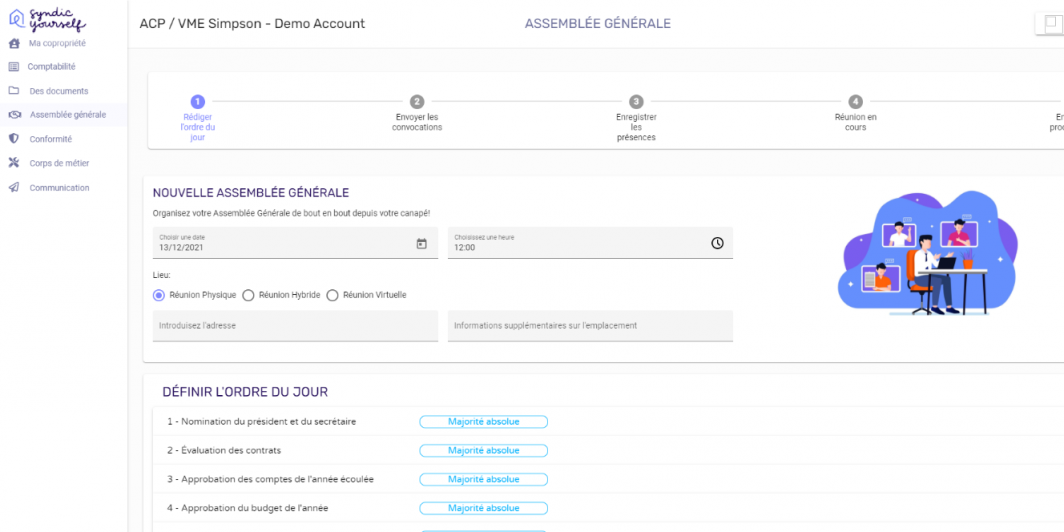

NEW OPTION « Comptabilité »

Nos clients nous aiment

Comme syndic non-professionnel j’avais besoin d’expertise, soutien et outillage afin de professionnaliser mon ACP. Je remercie l’équipe qui est à l’écoute, accessible et sympathique.

Syndic Yourself nous a offert une flexibilité, une transparence et une rapidité d’action dont toutes les copropriétés ont besoin. Syndic Yourself est l’outil idéal pour tout type de copropriété, petite, moyenne, etc, à essayer sans attendre !

Comme pour tant d’autres utilisateurs, il m’est apparu évident que Syndic Yourself est un soulagement pour les nombreux syndic de copropriété qui se sont occupés de la gestion de la copropriété.

Comparaison entre le syndic de copropriété professionnel, bénévole et Syndic Yourself… on vous laisse juger !

|

Syndic Yourself |

Syndic Bénévole |

Syndic de Copropriété Professionnel |

|

|---|---|---|---|

| Coût | |||

| Coût | 5€/mois : accès à la plateforme complète de Syndic Yourself |

Rémunération possible par la copropriété. + |

Entre 30€ et 40€/mois, coût moyen pour un syndic professionnel. + |

| Transparence | |||

| Transparence |

Transparence maximum + |

Dépend du syndic bénévole + |

Souvent absente + |

| Disponibilité/réactivité | |||

| Disponibilité/réactivité |

Réactivité et communication simple + |

Dépend de la disponibilité du syndic bénévole + |

Dépend du syndic professionnel + |

| Information vis-à-vis de la loi | |||

| Information vis-à-vis de la loi | Accès à l'ensemble des lois et règles qui régissent la copropriété |

Le syndic bénévole doit se renseigner + |

Responsabilité du syndic professionnel + |

| Temps et energie | |||

| Temps et energie |

Multitude de fonctionnalités qui font gagner du temps + |

Dépend des connaissances du syndic bénévole + |

Tout vous sera facturé + |

| Assistance | |||

| Assistance | Experts à votre disposition pour vous aider en cas de doute/question | En tant que syndic bénévole, vous ne disposez pas d'assistance. |

Attention aux suppléments + |

| Accès aux documents de la copropriété | |||

| Accès aux documents de la copropriété |

La plateforme regroupe tout. + |

Le syndic bénévole doit s'organiser + |

Responsabilité du syndic de copropriété professionnel + |

Syndic Yourself vous sauve et résout tous vos problèmes

Vous payez très cher votre syndic de copropriété professionnel mais vous ne savez pas vraiment pour quoi 💶

Votre syndic professionnel met du temps à réagir et à réaliser vos demandes ⏱

En tant que syndic bénévole, vous ne vous en sortez pas avec la comptabilité de votre immeuble 🧮

En tant que syndic bénévole, vous avez du mal à vous maintenir à jour vis-à-vis des lois et règles de la copropriété 🤷🏽♂️

En tant que syndic bénévole, j'ai plein de questions et je me sens seul dans ma mission 😔

Votre copropriété est-elle en règle aux yeux de la loi ?

Les normes évoluent continuellement… Votre immeuble est-il conforme avec les règles et lois en vigueur?

En fonction de votre résultat au test, vous recevrez par e-mail une checklist contenant des trucs et astuces pour vous mettre en conformité !

On parle de nous

Demandez votre offre gratuite !

- Un expert prend contact avec vous dans la journée (entre 9h et 18h)

- Il vous présente notre solution, en fonction de vos besoins

- Il vous remet une offre personnalisée